DSP TAX SAVER ICICI PRU LONG TERM EQUITY AXIS LONG TERM EQUITY SBI MAGNUM TAX GAIN HDFC TAX SAVER RELIANCE TAX SAVER FRANKLIN INDIA TAX SHIELD L&T TAX ADVANTAGE

The ELSS category is very competitive. It comprises a motley mix of funds with strong and established strategies. Funds that fall under this category are diversified equity funds with no restriction on the market cap. So they could be multi cap or large cap or mid cap oriented. Equity Linked Savings Schemes, or ELSS, fall under Section 80C of the Income Tax Act. Investments made here are eligible for a deduction up to Rs 1,50,000.

DSP Tax Saver Date of Analysis: March 2019 Analyst Rating: Neutral Fund Manager: Rohit Singhania The fund’s gestation period will be longer in a more competitive category with strong and established strategies. There have been significant changes within the investment team as well as at the fund-house level. In May 2018, BlackRock and DSP parted ways from their decade-old joint venture. The equity investment team also witnessed significant turnover, with some of its key managers– S. Naganath (CIO), Anup Maheshwari (CIO of equities after Naganath), and Harish Zaveri– exiting the fund company between 2017 and 2018, which is a cause for concern. The fund’s strategy, however, has stayed consistent under Singhania. He runs it in line with its investment mandate, which allows him to adopt a fluid investment approach without any bias or restrictions in terms of stocks or sectors. In the manager’s own words, this fund doesn’t have a defined investment approach, which in turn provides him the liberty to capitalise on any investment opportunity that he sees in the market, provided it makes a grade on his selection parameters.

Consequently, the fund’s portfolio turnover tends to be on the higher side.

While an unconstrained process can be very rewarding, it is risky, too. A wrong bet can lead to significant under performance. Also, the absence of a rigidly defined method means investments are made on a somewhat intuitive basis. Hence, it must be noted that the success of the investment process largely depends on Singhania’s execution skills.

We believe that the fund is yet to make a cut for itself within the category and needs more time before it could qualify for an upgrade.

ICICI Prudential Long Term Equity Date of Analysis: November 2018 Analyst Rating: Neutral Fund Manager: Sankaran Naren, Harish Bihani

There has been another change in manager in this fund. After taking over its mantle in October 2015, George Herber Joseph has relinquished the fund’s management responsibility effective November 5, 2018.

This fund has passed through multiple hands in the past few years. CIO Sankaran Naren (October 2005 till February 2011), Munzal Shah (March 2011 till May 2011), and Chintan Haria (June 2011 till September 2015) have managed this fund earlier. George Herber Joseph started comanaging this fund along with Haria from April 2015 and took over as the lead manager in October 2015. He comes from ICICI’s portfolio-management-services division.

The following report was based on our opinion on Joseph and his investment style.

Pleasingly, and despite the changes, the investment strategy largely stays the same. However, within the defined framework, Joseph has realigned the portfolio since taking over the fund in line with his investment thesis and understanding of macroeconomic scenarios. Joseph plies a free-flowing multi-cap strategy and follows a benchmark-agnostic approach for constructing the portfolio. He is fairly valuation-conscious and stays away from expensive stocks/sectors. He scouts for companies having good management with strong long-term track records, good free cash flow generating capabilities, and strong balance sheets. While investing, Joseph prefers staying away from investing in highly leveraged stocks.

Admittedly, the fund hasn’t done badly despite the changes at the helm, with the year 2017 being an exception. This year, the fund underperformed substantially as the manager’s valuation-conscious investment approach and strategy of taking contra bets has been out of favour, which dragged its overall performance under Joseph’s stewardship down with regard to benchmark index and category peers. However, these are still early days for Joseph at the helm here. We would like to evaluate his ability in executing the process over a market cycle to build conviction.

LIC is introducing its new offline term life insurance LIC’s Jeevan Amar (No.855) from 5th August, 2019. It is claimed that it is going to be one of the best cheapest term life insurance plan designed by LIC. Let us see the benefits and how it is beneficial for all of us.

Note:-Along with this plan, LIC also launched an online term life insurance and read more about this at “LIC’s Tech-Term (No.854)

LIC’s Jeevan Amar (No.855) is a Non-Linked, Non-Participating Term Life Insurance Plan. After a long gap, LIC launching a term life insurance. It is mainly because of the competition in this field of product.

Under this plan, there two categories of premium 1) Non-Smoker and 2) Smoker Rates. You can choose anyone option. However, if you have chosen the Non-Smoker category, then you have to undergo the additional medical examination like Urinary Cotinine Test. Based on the findings of the Cotinine Test, the premium will be applicable for Non-Smoker proposer.

LIC’s Jeevan Amar (No.855) – Features

# It is an OFFLINE Term Life Insurance from LIC.

# Minimum Sum Assured is Rs.25 lakh and there is no limit for maximum sum assured.

# You can pay the premium as regular, single or limited.

# You can opt for a level sum assured, where the sum assured you opted will remain the same throughout the policy period.

# You can opt for an increasing sum assured also, where the death benefit will remain the same up to 5 years of the first policy period. After that, it will increases at a rate of 10% for the next 10 years (up to it will turn double of the basic sum assured). From the 16th year, it will remain the same i.e double of the basic sum assured.

# Death Benefits can be taken in installments also of 5 years, 10 years or 15 years.

# Coverage up to 80 years of age.

# You can opt for Accidental Rider also.

# Lower rates for Non-Smokers and special rates for women.

# For regular premium policies, there is no surrender value as it is a term life insurance. However, for a single premium policy and limited premium policy, the surrender value is calculated based on the formula set by LIC.

LIC’s Jeevan Amar (No.855) – Eligibility

Let me share with you the eligibility for buying LIC’s Jeevan Amar (No.855).

LIC’s Jeevan Amar (No.855) – Premium

I have limited information about this policy. However, I have received this below premium example.

LIC’s Jeevan Amar (No.855) – Death Benefit Options

Death Benefit Sum Assured

As I have mentioned in the above post, there are two death options under LIC’s Jeevan Amar (No.855). You have to choose the type of death benefit sum assured option at the time of buying only. You can’t change the option in the middle of the policy period. They are as below.

# Level Sum Assured

Your nominee will receive the Sum Assured you opted while buying the policy. It will remain the same throughout the policy period.

# Increasing Sum Assured

Under this feature, your sum assured increase as below.

Under this feature, the death benefit will be the same as that of the initial sum assured you have chosen for the first five years.

From 6th policy year to 15th year, it will increase at the rate of 10% per year till it becomes the double of the basic sum assured. The increase in the sum assured will continue under an inforce policy till the end of the policy term, till the date of the death of the policyholder or till the 15th year, whichever is earlier.

From 16th policy year, the sum assured payable at death will be constant and i.e double of the sum assured you opted initially.

As per the chosen option, your nominee will receive the death benefit during which period of the policy your death occurs.

Death benefit payment option to the nominee

Your nominee can receive the death benefit as a lump sum or in installments. If you opted for installments, then LIC will pay the death benefit installments in 5 years, 10 years or 15 years.

You can choose the full death claim amount be payable in installments or a certain portion of death claim in installments.

You can choose this installment option either at the time of buying or during the policy period.

The installments will be payable to nominee in advance at yearly or half-yearly or quarterly or monthly as one has opted for. But make sure that these minimum installment payment rules.

For monthly payment, the minimum installment amount is Rs.5,000.

For quarterly payment, the minimum installment amount is Rs.15,000.

For half-yearly payment, the minimum installment amount is Rs.25,000.

For yearly payment, the minimum installment amount is Rs.50,000.

If the net claim amount is less than the required amount payable in installment, then LIC will pay as a lump sum one-time payment to your nominee.

LIC’s Jeevan Amar (No.855) – Review

Considering the market competition in online term life insurance plans, LIC launched this plan with the utmost care and including the many features which are already available in the market.

# It is an OFFLINE term life insurance. Hence, the premium will be higher than their newly going to be launched plan LIC’s Tech-Term (No.854). Also, it looks upfront that LIC’s Jeevan Amar (No.855) premium is much cheaper than it’s earlier offline term life insurance. Hence, it is a big benefit for those who are desperate to buy the term life insurance from trusted LIC. However, I strongly suggest you to buy it online. Because agents commission under this plan is 25% for 1st year, 7.5% in 2nd and 3rd year, 5% in subsequent years (for the policy period of 15 years or more). Hence, why not pay more than opting the same from the online?

# Coverage of the policy is up to 80 years of age. Even though Life Insurance is not required up to 80 years of your age, but LIC added this feature to compete with private players. Hence, this is an attractive move.

# This plan comes with an accidental rider. It’s an earlier version of term life insurance was without any rider. Hence, this time LIC added accidental rider benefit. This is one more positive.

# Special discounts for a female is unique and attractive to all-female who are looking for online term life insurance from LIC.

# Premium paying option is too flexible with options like Single, Limited Period and Regular Period. This gives us flexibility.

# Increasing Sum Assured option is first time added by LIC. Where for the first 5 years it will not increase. However, after 5th year to 15th year it will increase at the rate of 10% (up to this increasing sum assured double the basic sum assured). From 16th years onward, it will remain the same throughout the policy period. This is the big relief for those who have to review their life insurance coverage and avoid having multiple life insurance products. However, keep one thing in mind that the maximum benefit one avail under this plan is DOUBLE of basic sum assured you availed at the start of the policy period. Hence, consider the actual need and take a call.

BUT WHY IS LIC LAUNCHING AN OFFLINE PRODUCT WITH the SAME FEATURE, WHEN IT JUST LAUNCHING ONLINE TERM LIFE INSURANCE WITH THE SAME FEATURE?

IS IT JUST TO CATER TO THEIR AGENTS FORCE? OR THOUGHT OF TO CATER TO THOSE WHO ARE NOT WELL VERSED WITH ONLINE BUYING? I DON’T THINK SO. BECAUSE WITH THE KIND OF SMARTPHONES, ONLINE BUYING AND ONLINE PAYMENT THE PEOPLE ARE ACCUSTOMED, IT IS USELESS TO BUY COSTLY OFFLINE PLAN WITH THE SAME FEATURE OF ONLINE (except lower minimum sum assured).

I strongly suggest you go for online term life insurance LIC’s Tech-Term (No.854) rather than this offline product.

Call or whatsapp @9891423442 or visit www.agindiaonline.com

LIC one of Best Plan LIC JEEVAN LABH. If you believe only in LIC then Jeevan Labh is one of Best Plan in LIC. Bonus rates etc.. are very attractive. Very important that Limited premium option will give you more benefits.

LIC Jeevan Labh – In Short

LIC Jeevan labh is a non linked, limited premium, with profit endowment assurance plan. The limited premium feature in this plan lets you chose among 3 variants of Policy terms, and corresponding Premium paying terms. Available Policy terms are 16, 21 and 25 years, and premium paying terms are 10, 15 and 16 respectively.

Once you decide on which policy term you want to invest in for, you will be intimated with the premium you have to pay, which further depends on age of the person to be insured and sum assured opted for.

You keep paying the premiums for defined premium paying term, and stay invested till policy term, then you will get maturity benefit as Sum assured plus all accrued reversionary bonuses and final additional bonus ( If any). Unfortunately if you die before completion of policy term, then your policy nominee will receive the Sum assured plus all accrued reversionary bonuses.

If your policy premium is 10% or less of the policy sum assured then your premiums are eligible to be claimed under section 80C benefit and also the maturity amount you get will be tax free u/s 10(10)d.

LIC Jeevan Labh – Basic features

Minimum Entry Age – 8 years

Maximum Entry age – 59 years

Maximum Maturity age – 75 years

Minimum Sum assured – Rs 2 lakh

Maximum Sum assured – No Limit

Policy terms (Years) – 16, 21 and 25

Premium Paying Terms (Years) – 10,15 and 16

LIC Jeevan Labh – Other additional Features

This policy provides one optional rider as Accidental death and disability benefit, by payment of additional premium. If opted, the total basic sum assured on accidental death will get doubled and in case of permanent total disability (due to accident), all future premiums will be waived and sum assured equivalent amount will be distributed in 10 monthly installments.

There’s also option for term insurance rider, which one opts for at the time of policy buying. This will increase the death benefit with the sum assured opted for, under term insurance rider.

Loan facility is also available in this plan subject to few conditions.

Discounts on Premiums are available on different Premium payment modes and on high sum assured.

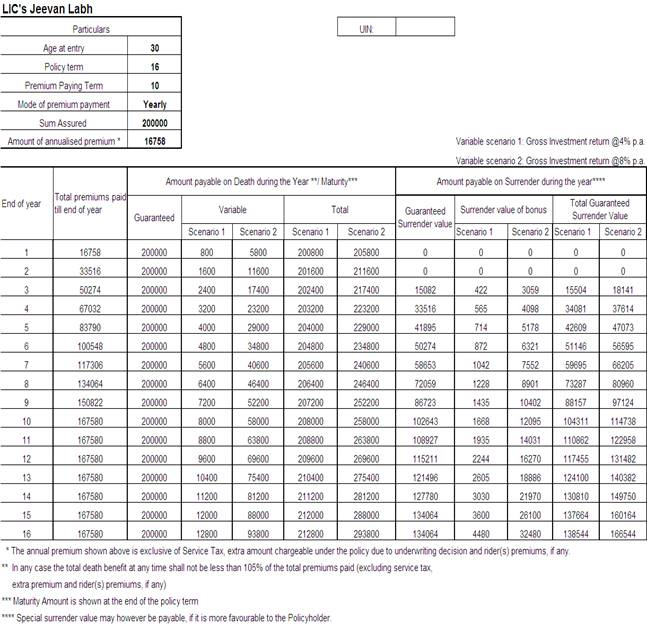

LIC Jeevan Labh – Returns review

Let’s analyse the illustrations provided on LIC website to figure out the tentative returns from LIC Jeevan labh. Since this is an endowment plan which invests only into debt instruments, so we can’t expect equity like returns in this product. IRDA has also stipulated to show the illustrations with 4% and 8% returns.

On maturity, insured will get sum assured plus simple reversionary bonus plus final additional bonus. Simple reversionary bonus is declared every year, and depends on the corporation’s overall performance in that particular year. The bonus rate varies with different policies and term with in the policy.

The above illustration is for 30 years old person , who opted for 25 years policy term with 16 years of Premium payment term. For sum assured Rs 2 lakh the premium comes out to be Rs 9134 (exclusive of service tax).

On Maturity the policy holder is expected to get Rs 220000 (@4%) and Rs 370000 (@8%). Premium has to be paid for 16 years and policy will be matured after 25 years. Calculating IRR as per the data , it comes out as 2.33% and 5.28% respectively. It will reduce further when Service tax is added to the Premium

The above illustrations is for 30 years old, with 10 years premium paying term and 16 years policy term. IRR comes out to be as 2.08% (@4%) and 4.91% (@8%). Returns will further reduce when Service tax added to premiums.

The actual returns of the policy may vary. Even the previous bonus rates of LIC policies are better than shown in illustrations. But still one should not expect much of difference, being a debt product.

LIC Jeevan Labh – Should you invest?

Well, first thing first, getting adequate insurance cover from endowment policy will prove very costly to you. So you have to buy Term Insurance if you want to have good coverage. Thus, the buying insurance through this product is out of question here.

Looking at the expected returns, if you are happy with 5-6% of annualized returns then yes this policy is for you. But do remember that the return will be less for aged investors as the mortality costs will be high, but also returns will improve slightly for those who claim tax benefit u/s 80C.

Whether the policy work for you or not will depend on your age, your risk profile, your cash flow, your other investments and insurance coverage, your Required Asset Allocation and goals targeted. There cannot be a simple yes or no to this. No product is good or bad, it’s the usage and fitting of that product into the financial plan which makes it useful.

On the face of it since it is a lock in product, with no re-balancing feature and no control on managing the funds, with unnecessary insurance cost ( as term plans are already bought), so I advise not to invest just because it is from LIC. I have always been advising to keep Insurance and Investments separate, as i find the structure easy to manage.

Do the maths, understand it’s usefulness in your financial profile, look at your finances holistically and then decide.

More call or whatsapp @ 9891423442 or visit www.agindiaonline.com

Today in Investment market every one is coming with Online Transaction Platform, Like- PayTm, Grow, ETmoney, Every AMC with online app/portal.

So it very important to know which platform and why, you have to choose

MFU- Mutual Fund Utility

MF Utilities India Pvt Ltd (MFUI) is the Mutual Fund Industry’s “Shared Services” initiative formed by the Asset Management Companies (AMCs) of SEBI registered Mutual Funds under the aegis of AMFI, with an objective of investor empowerment, distributor / RIA convenience, consolidation of information to various agencies, operational efficiency for RTAs and benefits to AMCs, thereby benefitting all stakeholders in the industry. The prime objective of MFUI is to consolidate all “Transaction Requests” received by the industry from multiple sources and transmit it to the “Fulfiller” of the request (Transfer Agent), thereby bringing in operational efficiency by reducing multiplicity and duplication of activities. Towards achieving this objective, MFUI has developed the Portal, MF Utility (MFU), which operates as a “Transaction Aggregating System” for transactions in Mutual Funds.

MF Utility (MFU) is an innovative initiative of the Indian Mutual Fund Industry that brings significant benefits to all stakeholders, i.e. Investors, Distributors, RIAs and Asset Management Companies, by leveraging technology, MFU will bring many conveniences to the investors and distributors /RIAs and allow Mutual Funds to significantly enhance their reach and presence in the country to further the goals of retail penetration. MFU will also help remove duplicities in the system and reduce the inherent risks in the industry.

MFUI is equally owned by the AMCs of SEBI registered Mutual Funds in India.

Benefitsof MFU vs Other Platforms

MFU- MF Utility

PrivatePlayer

1- Not Chargeable

Chargeable/Partially Chargeable

2- Life Time Free

Short time free for attract customers

3- Owned by AMC/SEBI

Owned by private company/person

4- Not to be close

May be close at any time

5- View all your portfolio of all AMC

Only view folio of investment from his portal

6- Transact all folio at industries

Very limited option

7- Easy to enroll

Depend on others source etc

Editor View

Therefor my personal recommendation to don’t go with Private Players, As they have personal interest and they may be charged after certain time, which will give you panic situation in between of your investment.

for more you can call/whatsapp @ 9891423442 or visit www.agindiaonline.com, https://youtube.com/c/Aginvestment

There are different Types of Mutual Funds for SIP that include equity, debt, balanced and ultra-short term funds.

However, Equity Mutual Funds offer maximum returns when invested via a SIP. Financial advisors suggest that the investors must invest in best mutual funds for SIP basis their investment objectives and the period of SIP investment.

Why Invest in Top Ten SIP Funds?

SIPs give a disciplined approach to investing Systematic investing helps in financing the future dream and major goals like- retirement, child’s career, purchase of a house/car or any other assets SIPs help in making the most of compounding and are ideal for young investors Systematic Investment Plans minimize the risk of equity fluctuations.